The Home of Capital Cycle Investing

Marathon invests according to the capital cycle: a framework that describes the relationship between the return on capital invested in a business, the actions of management, and the valuation of that company's equity by outside investors.

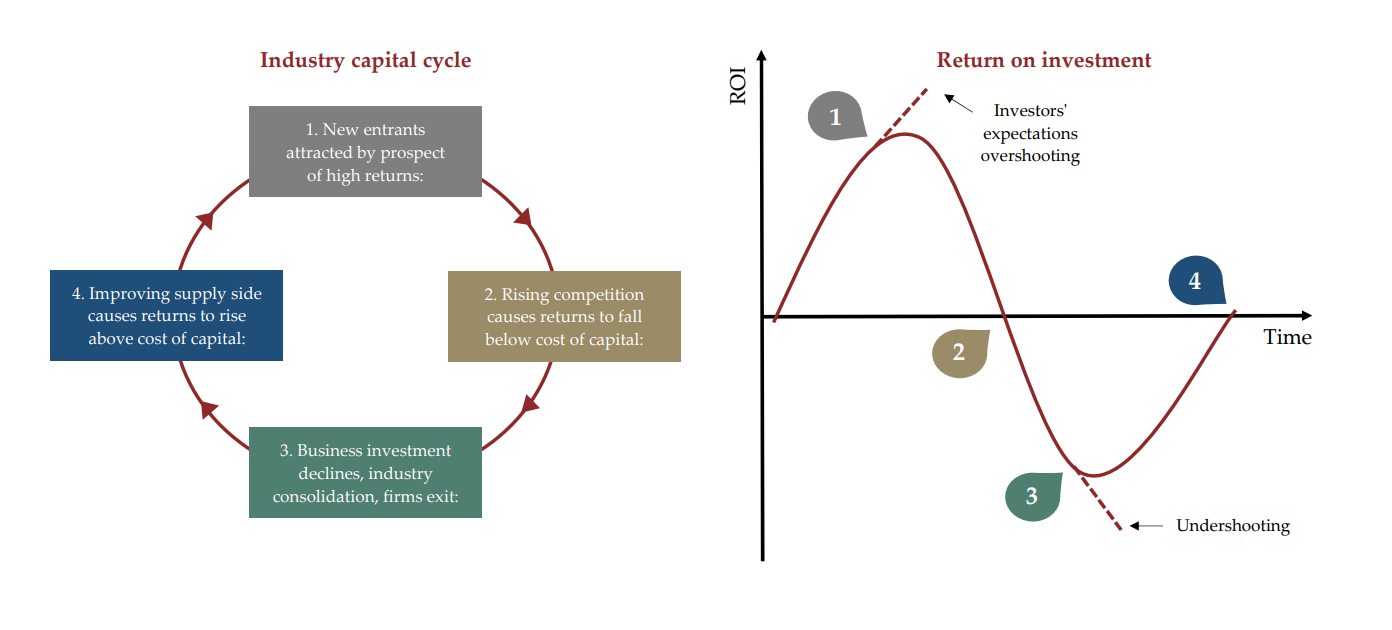

Two simple ideas about how capitalism works in the long run have always been paramount.

The first is the observation that high returns in industries tend to attract capital and competition, just as low returns repel them. The resulting ebb and flow of capital affects long-term returns for shareholders in often predictable ways, what we call the capital cycle. Since high levels of investment tend to be detrimental to shareholder returns over the long run, Marathon seeks to invest in companies where high returns are sustained by barriers to entry deterring investment or companies with low returns in industries where investment is declining.

The second guiding idea is that management skill in allocating capital is vital over the long-term. The best managers understand and seek to alter the capital cycle in their industries through sensible reinvestment choices. Decisions about new capital projects, acquisitions or disposals, and equity issuance or buybacks are critical to the ultimate outcome for shareholders.

The capital cycle is a framework that allows Marathon to anticipate changes in profitability and equity valuation over the long-term. It is neither traditional ‘value' nor ‘growth' investing but lends itself to contrarianism and extended long-term holding periods.

The investment team uses fundamental, bottom-up qualitative analysis to evaluate businesses and the industry within which they operate. In-depth, internally-generated research is a distinguishing feature of Marathon's investment process; the research is focused on industry capital cycle characteristics and company management's motivation, incentivisation and skill at responding to the forces of the capital cycle.

Marathon broadly characterises investments within two opposite points of the capital cycle:

- High return phase (top half of the capital cycle): where high rates of return within a business and/or industry are being attained, often due to intangible asset(s) that allow them to fend off competition and excess capital that would otherwise be drawn to the prospects of high returns. Typically, a consolidated industry market structure with high barriers to entry.

- Depressed return phase (bottom half of the capital cycle): where rates of return have fallen to or below the cost of capital and where capital is being repelled as a result. A consolidating industry market structure, where supply and competition are removed, or a radical shift in management strategy, are often conditions leading to making these types of investments.

Sustainability

As an active long-term investor, sustainability has always been an integral part of Marathon’s investment decision-making process. Marathon’s primary objective – the fiduciary duty to add value within clients’ agreed risk parameters – is enhanced by considering material sustainability issues. Please click here for more information.

Marathon’s current Sustainability & Climate Report can be found here.